The long awaited Main Street Lending Program (MSLP) officially became available to eligible borrowers on June 15, 2020. Aimed to help small and mid-sized U.S. businesses obtain credit to alleviate the economic difficulties caused by the various COVID-19 pandemic-related shut downs, reopenings, and recovery, the MSLP may prove beneficial for many businesses. Originally announced on April 9, 2020 as part of the C.A.R.E.S. Act, the program has received various updates to expand loan eligibility, alter loan amounts, and offer greater flexibility on repayment terms. As part of the June 8, 2020 updates to the MSLP, the minimum loan amounts were lowered for each type of facility, collateral exceptions were clarified, and repayment terms were expanded. The deferral period for principal payments was increased to the end of year two and interest payments are deferred for one year for all facilities.

The MSLP provides businesses that were in sound financial condition prior to the COVID-19 pandemic with the opportunity to apply for a loan through an eligible lender using one of three loan facilities:

- Main Street New Loan Facility (MSNLF)

- Main Street Priority Loan Facility (MSPLF)

- Main Street Expanded Loan Facility (MSELF).

Eligible lenders will accept and review borrower applications, conduct underwriting diligence and, to the extent all criteria of the MSLP and eligible lender are met, directly fund the loan to the borrower. For borrowers, understanding that the loans are extended by an eligible lender is important, because the borrower must meet the underwriting guidelines that such lender has in place and the criteria of the type of MSLP facility that best suits its needs. Since potential borrowers need to meet the conditions of the MSLP and the underwriting guidelines of the lender, it will be possible for some borrowers to be eligible for the loan facilities, but be declined for the loan by the lender.

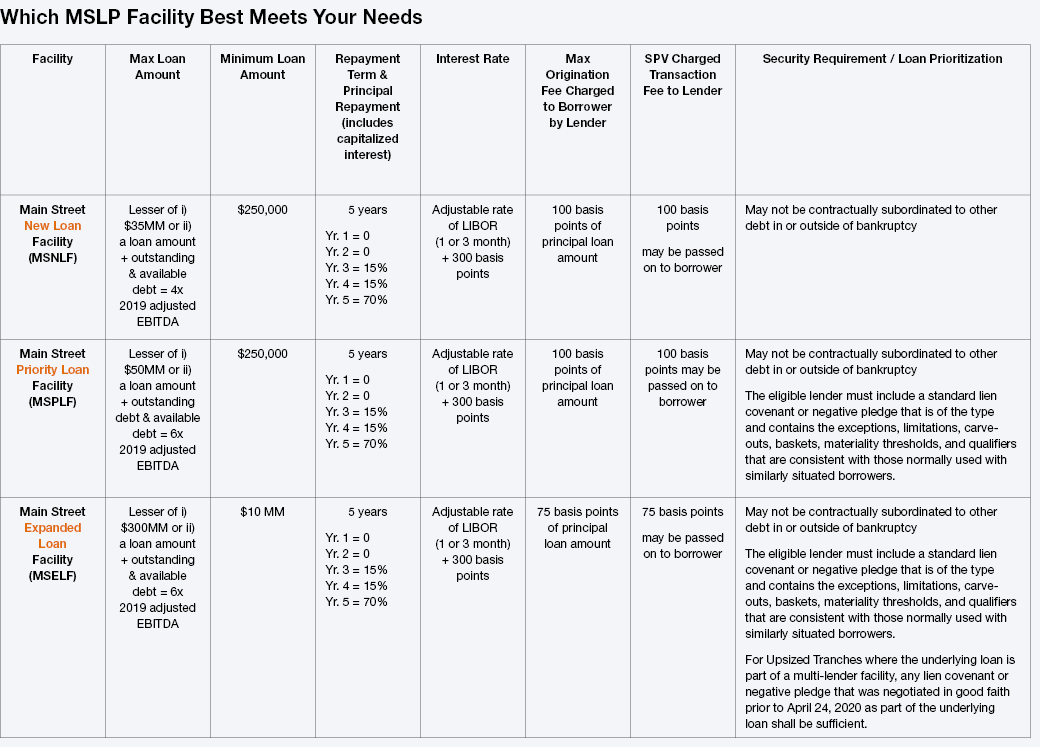

Each borrower will need to determine which of the three MSLP facilities best meets the needs of their business. While there are clear similarities between the three facilities, there are also important differences. Collateral coverage, loan purpose, and maximum loan amounts (as shown in the below chart) distinguish the MSNLF, MSPLF, and MSELF facilities from one another and should be considered by each borrower.

Definitions:

Who is an eligible borrower?

Eligible business borrowers must satisfy each of the following conditions:

- 15,000 employees or less, OR 2019 revenues of $5 billion or less;

- Established prior to March 13, 2020;

- Is not an ineligible business as defined by the SBA;

- Has not received specific support pursuant to the Coronavirus Economic Stabilization Act of 2020 (Subtitle A of Title IV of the CARES Act). NOTE, receiving a PPP loan does not disqualify a business from participating in the MSLP;

- Is a business formed in the United States of America or created under the laws of the U.S. with significant operations and a majority of employees based in the U.S.;

- Been in sound financial condition prior to the COVID-19 pandemic;

- Only participates in one MSLP facility and must not participate in the Primary Market Corporate Credit Facility;

- Makes all of the certifications and covenants required under the MSLP; and

- Makes commercially reasonable efforts to retain workers and maintain payroll.

What are eligible lenders?

Eligible lenders are U.S. federally insured depository institutions, a U.S. branch or agency of a foreign bank, a U.S. bank holding company, a U.S. savings and loan holding company, a U.S. intermediate holding company of a foreign banking organization or a U.S. subsidiary of any of the foregoing.

How are total employees and revenue calculated?

Employee Count

- Determine the number of employees by using the average of the total number of persons employed by the Eligible Borrower and its affiliates for each pay period over the 12 months prior to the origination or upsizing of the MSLP loan.

- Uses the SBA’s regulation to include all full-time, part-time, seasonal, or otherwise employed person including employees of affiliates. Independent contractors are excluded from the count.

No exceptions are made for restaurant and hospitality companies

Revenue

- For MSNLF and MSPLF, the lender will calculate the borrower’s 2019 adjusted EBITDA by using a methodology they used previously when extending credit to the borrower or to similarly situated borrowers on or before April 24, 2020.

- For MSELF, the lender will calculate the borrower’s 2019 adjusted EBITDA by using a methodology they used previously when originating or amending the underlying loan on or before April 24, 2020.

- Calculated using one of the two methods for each borrower and its affiliates based on what is normal and customary for such borrower and/or what is accepted by the eligible lender to qualify the loan:

- 2019 GAAP based audited financial statements, or

- 2019 annual receipts as reported to the IRS.

Resources:

- Federal Reserve Bank of Boston MSLP Overview

- Information for Borrowers from Federal Reserve Bank of Boston

- Information for Lenders from Federal Reserve Bank of Boston

- FAQs

- MSLP Forms and Agreements

The information provided in this alert, including the chart and definitions below, is based on the June 8, 2020 updates to the MSLP provided by the Federal Reserve Board and the U.S. Department of the Treasury. It is acknowledged that this information may change based on future updates.